Jumbo Roth IRA – 05/01/16

![]()

Money Matters – Skloff Financial Group Question of the Month – May 1, 2016

By Aaron Skloff, AIF, CFA, MBA

Q: Because I earn $300,000 per year I am disqualified from contributing to a Roth IRA. Are there other ways to accumulate Roth IRA savings?

The Problem – Higher Earners Disqualified from Contributing to Roth IRAs

Roth Individual Retirement Accounts (IRAs) are highly desirable to retirement savers because they allow for growth on a tax free basis, withdrawals on a tax free basis and are exempt from required minimum distributions (RMDs). Unfortunately, the IRS imposes income limits on those looking to contribute to Roth IRAs. In 2016, the income phase-outs limits are from $117,000 to $132,000 for single filers and $184,000 to $194,000 for those married and filing jointly. Translation: if you earn more than $132,000 as a single filer or $194,000 as a joint filer you cannot contribute to a Roth IRA.

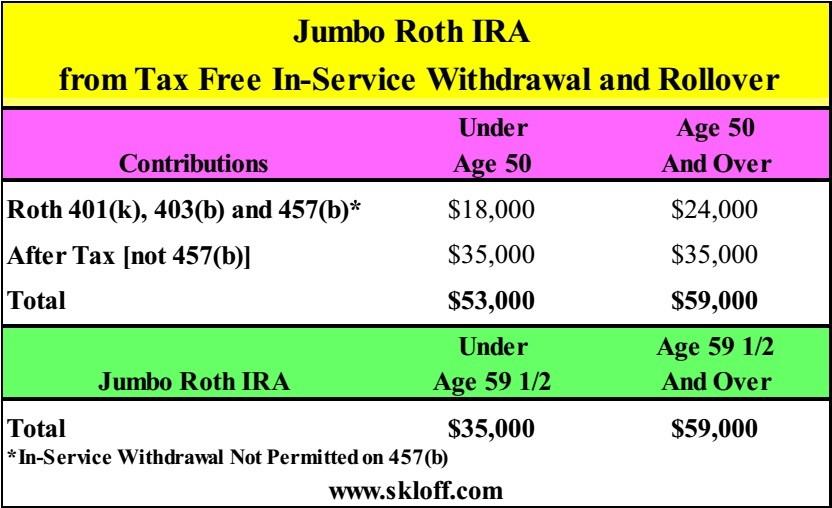

The Solution – 401(k), 403(b) and 457(b) Roth Contributions

Regardless of your income, you can contribute to a Roth 401(k), 403(b) or 457(b) retirement plan if your employer offers a Roth option.

Your contributions are limited to the lesser of your income or $18,000 (if you are under the age of 50) or $24,000 (if you are 50 or over).

Regardless of your income, you can also contribute to your retirement plan on an after tax basis if your employer offers an after tax option (not available on 457(b) plans). Your additional contributions are limited to the lesser of your income or $35,000.

The IRS imposes annual per plan limits on contributions. The combination of Roth, after tax and employer contributions cannot exceed $53,000 (for those under the age of 50) or $59,000 (for those age 50 or over). Note: employer contributions must be on a pre-tax basis.

Create a Jumbo Roth IRA with a Tax Free In-Service Withdrawal and Rollover

If you are under the age of 50 you can contribute a combined $53,000 to your employer plan ($18,000 Roth plus $35,000 after tax). If you are 50 or over you can contribute $59,000 ($24,000 Roth plus $35,000 after tax). You can then complete a tax free in-service withdrawal and rollover the after tax portion if under age 59 ½ to a Roth IRA or the entire amount if age 59 ½ and over, if your employer offers this option.

Fortunately, you can repeat this process every year. The following chart summarizes the process.

Click to Enlarge

Often Overlooked – Backdoor Roth IRA

In addition to the Jumbo Roth IRA described above you can also contribute another $5,500 (if you are under the age of 50) or $6,500 (if you are 50 or over) to a Backdoor Roth IRA.

Action Steps – Maximize Your Roth IRA Savings

Maximize your Roth IRA savings through Roth 401(k), 403(b), 457(b) contributions and after tax contributions, then complete a tax free in-service withdrawal and rollover. Lastly, enjoy tax free withdrawals for the rest of your life or avoid withdrawals completely and leave a tax free Roth IRA for your heirs.

Aaron Skloff, Accredited Investment Fiduciary (AIF), Chartered Financial Analyst (CFA), Master of Business Administration (MBA) is CEO of Skloff Financial Group, a Registered Investment Advisory firm. He can be contacted at www.skloff.com or 908-464-3060.

Click Here for Your Long Term Care Insurance Quotes